Need Technology Partner With Document Processing Automation?

We speak real estate. We’ve been developing software products for real estate for 2 decades. Speak to Ascendix consultant.

Underwriting is the very stage in lending when a single miscalculation or data entry error can cause irreversible financial losses for a lender. This process is known for its heavy paperwork and data entry demands, which can be time-consuming and prone to errors.

That is why automating this number-heavy process with a commercial underwriting platform is vital to ensure low financial risk, reduce the chance of human error, automate calculations to close deals faster, and increase the range of investment opportunities.

Here are some top commercial underwriting platforms available:

Underwriting in real estate transactions is the process of examining the finances of a loan applicant and their creditworthiness in order to check how much risk a lender will take if they issue that loan.

An underwriter is a financial risk expert, often working for a bank or any other financial organization, who reviews property appraisals and assumes the lender’s risk by analyzing the loan application and evaluating the borrower’s credit history and assets.

What are the common types of loans an underwriter assesses in commercial real estate?

Commercial real estate underwriting software or automated underwriting systems are digital solutions used by lenders, appraisers, and underwriters for the automation of processes like financial analysis and risk assessment.

They often incorporate machine learning mechanisms and artificial intelligence, as well as business rules manually defined by the underwriter, used to automatically collect and analyze borrower’s financials (credit history, income, due diligence documents, etc.) in addition to property-related data.

With real estate underwriting software, underwriting teams can ensure the whole process complies with external regulations. They can create workflows for the team and evaluate the viability of the deal with higher precision.

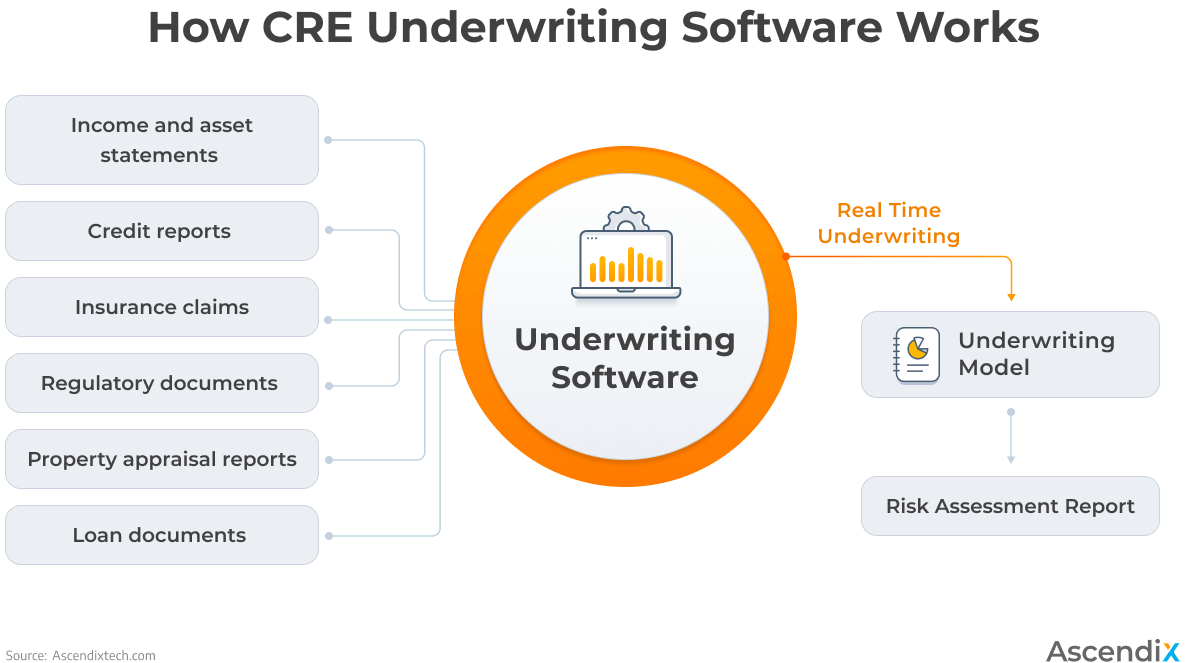

How CRE Underwriting Software Works

Underwriting in commercial real estate often feels like navigating a labyrinth of paperwork, where every document is a piece of the puzzle. This is where document abstraction comes into play—automating the extraction of key data, making the underwriting process not only faster but also more accurate.

This is a feature that allows underwriting software tools to connect to systems like Equifax, Experian, and TransUnion in order to access borrower’s credit and payment history, helping underwriters conclude whether the borrower is qualified for the loan.

It also helps underwriters access income and asset details like tax returns, payroll records, and investments to conclude whether the borrower is in a position to support the loan or provide collateral.

By accessing liabilities like credit card balances and debt history, underwriters can calculate the debt-to-income ratio and draw conclusions on the borrower’s ability to manage debt.

Document abstraction is a feature that helps automate the extraction of relevant information from complex documents. By using advanced technology to identify and pull-out critical data from loan applications and supporting documents, this feature significantly reduces the manual paperwork burden and minimizes errors.

A customer-portal is a web-based interface that provides borrowers and lenders with a centralized place for data storage and management.

This feature grants secure login sessions, allowing borrowers to upload loan-related data and documentation, receive notifications, and check the loan status without the need for one-to-one meetings with lenders in real life.

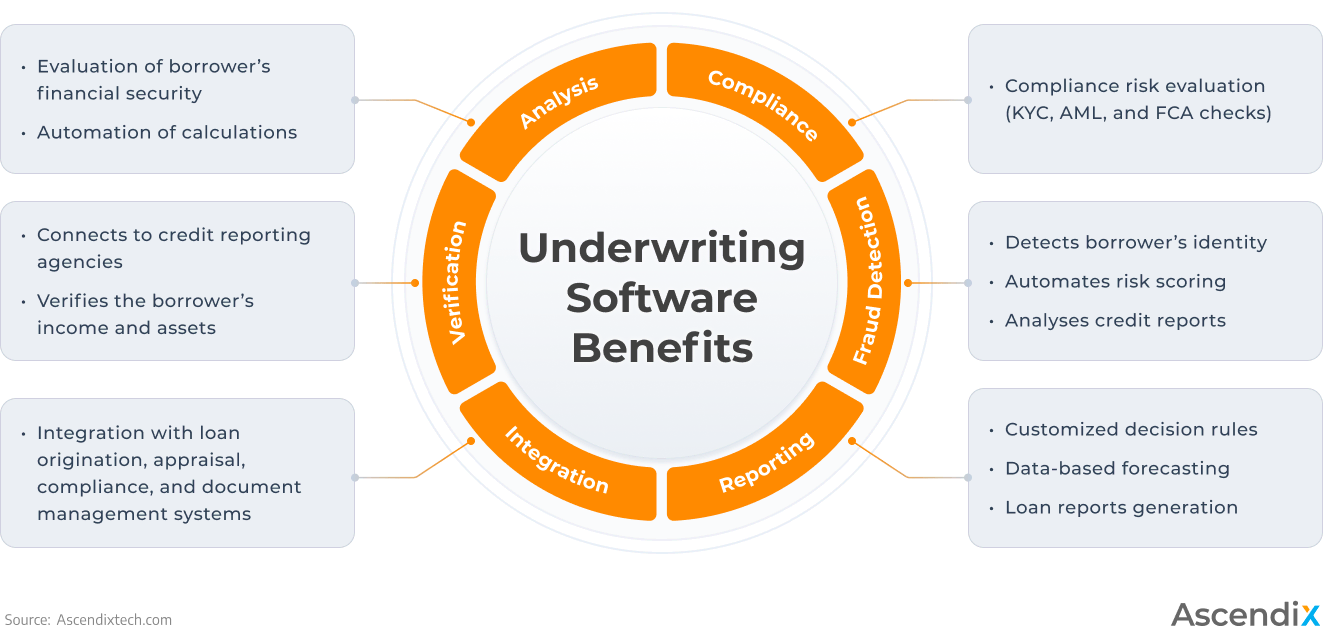

This feature helps underwriters ensure the CRE loan application process complies with industry regulations like Know Your Customer (KYC), Anti-Money Laundering (AML), and Fair Credit Reporting Act (FCA). With the compliance management feature, companies can assess their compliance risks and establish a proper level of due diligence.

With this feature, a system will flag any fraudulent activity. First and foremost, the system helps the user detect the borrower’s identity by checking their social security number and driver’s license or verifying their address for identity theft prevention.

Meanwhile, with credit report analysis and automated risk scoring, underwriters can check the borrower’s credit history and detect activities like unauthorized inquiries.

This is an underwriting software feature that allows users to ‘customize’ the initial decision rules and set new criteria for the loan evaluation.

A user can set a credit score threshold, debt-to-income, and loan-to-value ratio limit for the automatic approval or decline of loans. In other words, predetermined criteria enable users to manage loans that are automatically approved or declined by a system, a feature that reduces human error and saves time.

Real estate reporting features help underwriters gain insights into their loan portfolio, analyze its performance, assess the lender’s risks, and ensure that the loans comply with industry standards and regulations. Some underwriting solutions incorporate a forecasting feature as a part of analytics. Due to this feature, underwriters can forecast future loan performance based on historical data, contributing to the risk management of the entire loan portfolio.

The ability of the underwriting software to integrate with other systems is a must, since connectivity is a feature helping an underwriting system extract data from credit bureaus and verify borrower’s assets and income in systems like Plaid and FormFree respectively.

If an underwriting system integrates with other tools like loan origination, compliance, appraisal, and document management software, an underwriter can effortlessly streamline the loan origination process and document signing, check the correlation between the asset value and the loan to be borrowed while also ensuring the loan follows lending compliance regulations.

Underwriting Software Benefits

Most underwriting tools can integrate with credit reporting systems like Equifax, Experian, and TransUnion, automatically gathering financial data about borrowers-to-be (for instance, credit history), hence saving days on the research otherwise done manually.

The software also helps underwriters tackle mundane tasks like extracting due diligence data from property databases and financial statements with further analysis and review.

Underwriting tools also minimize the amount of time needed to generate documents (creating a document takes a few minutes), perform calculations, and assess lender’s risks.

Underwriting automation software sends real-time alerts and notifications on changes or mismatches that occur in property information databases, credit reports, and financial statements. Let’s say the borrower’s credit score drops. In this case, a system will send an alert to the underwriter, notifying them that a credit history review must be performed.

With built-in calculation mechanisms, underwriting software automates complex calculations like debt-to-income ratios, cash flow coverage ratios, and internal rate of return among many others, helping underwriters qualify borrowers.

We speak real estate. We’ve been developing software products for real estate for 2 decades. Speak to Ascendix consultant.

From now on, users can forget about multiple Excel sheets and documents scattered in different systems. All because most digital underwriting tools serve as underwriting platforms, meaning that all data is stored and managed in the same place without confusing duplicates and with simplified access.

It also streamlines tasks often performed manually like data collection, its entry, and processing, therefore automating workflows and reducing time.

Multifamily underwriting software helps underwriting professionals find more accurate expense and rent comparables, get real-time insights on market trends, and analyze the extracted data to identify patterns in real estate.

Having access to a wide range of accurate data like real-time market changes helps underwriters make a precise financial analysis and forecast on what returns investing in a particular property would be most profitable.

Automate time-consuming calculations to reduce human error and do things faster.

Selecting the right commercial underwriting software is crucial for efficient and accurate real estate evaluations. In this section, we’ll review 10 tools, each with distinct features designed to help you manage underwriting tasks effectively.

🔹Founded: 2017

🔹Location: Toronto, Canada.

🔹Pricing: to be enquired

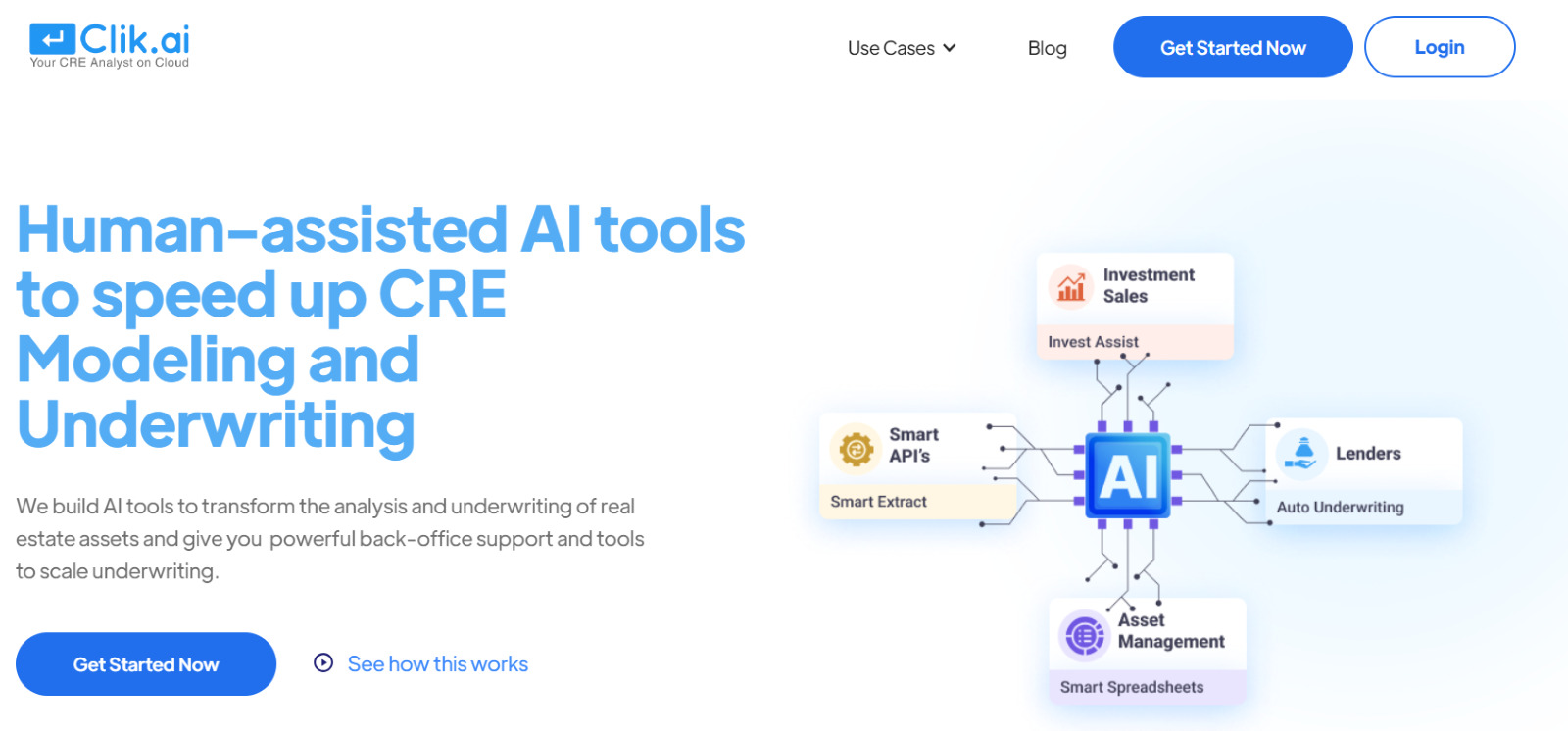

Clik.ai

Clik.ai is a multifamily underwriting software that helps underwriters effectively process deals and close them faster.

Clik.ai creates investment models by extracting data from documents like rent rolls, operating and trailing twelve months (T12) statements, and can even map the extracted data right into the company’s models.

Also, the user can create interactive graphics to track property portfolio performance and generate reports for the evaluation of acquisition and asset management.

| Features | Cons |

|---|---|

🔹Founded: 2016

🔹Location: Overland Park, USA

🔹Pricing: 14-day trial available, $275 per user (monthly subscription)

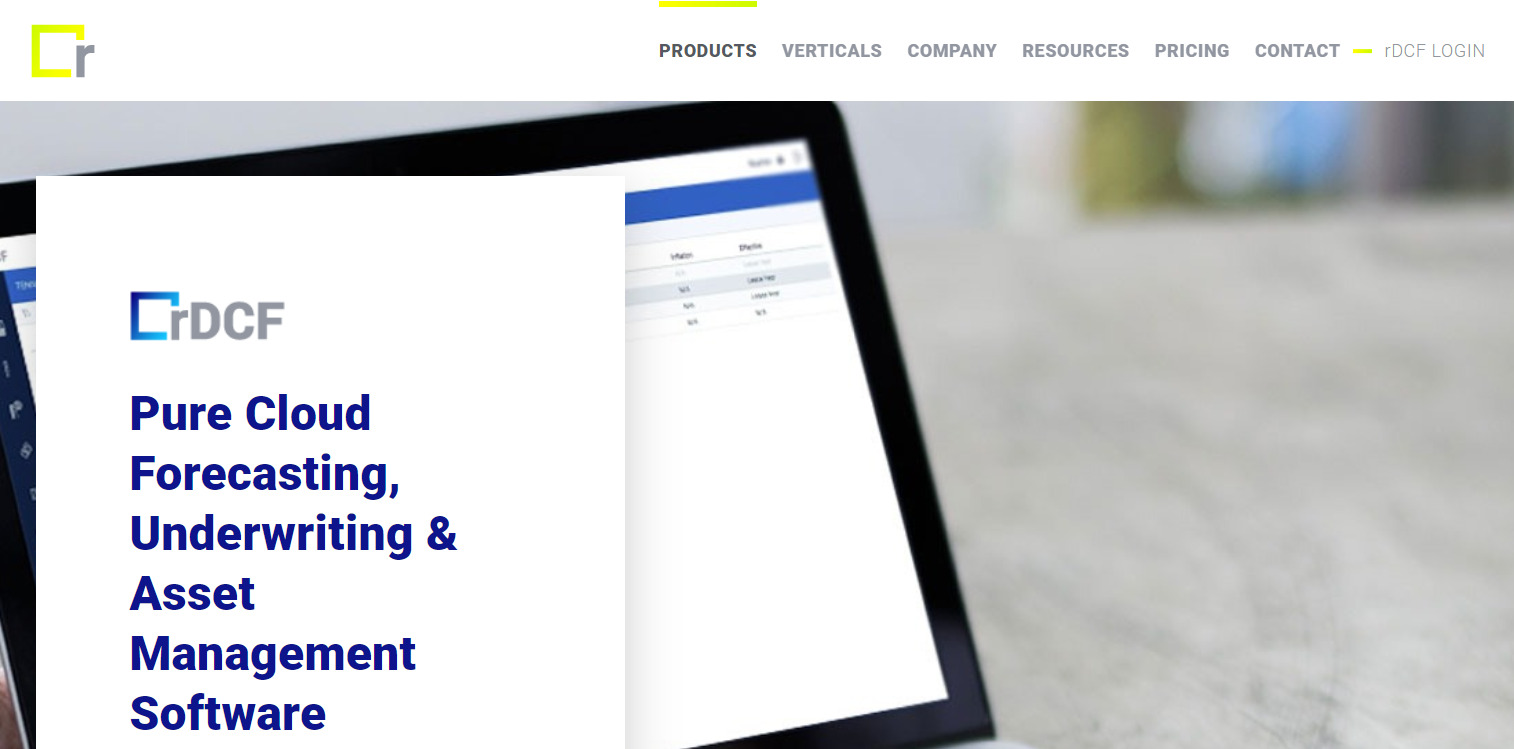

rDCF

rDCF is a cloud-based CRE underwriting software that helps a user build a flexible discounted cash flow (DFC) model for complex property appraisal and automate their CRE loan underwriting calculations.

With rDCF, a user gets such features as Excel-based reporting, debt and equity modeling, and built-in underwriting metrics.

The software reduces data input errors, offers quick and easy file sharing, and allows users to create ready-to-present reports that are generated in a matter of seconds.

| Features | Cons |

|---|---|

internet-connected device without installing software; | |

🔹Founded: 2016

🔹Location: Washington, USA

🔹Pricing: module-based pricing

RealINSIGHT

RealINSIGHT is a cloud-based commercial underwriting platform that helps companies make informed investment decisions with centralized data and interactive tools.

It integrates with other systems, allowing a user to store data in one place that acts as a single source of truth (SSOT) anyone in the company can access.

The commercial underwriting software automates workflows, offers reporting features, and builds up a database that a user can leverage in the future.

| Features | Cons |

|---|---|

🔹Founded: 2016

🔹Location: Chicago, USA

🔹Pricing: Pricing varies by users, features, and portfolio size

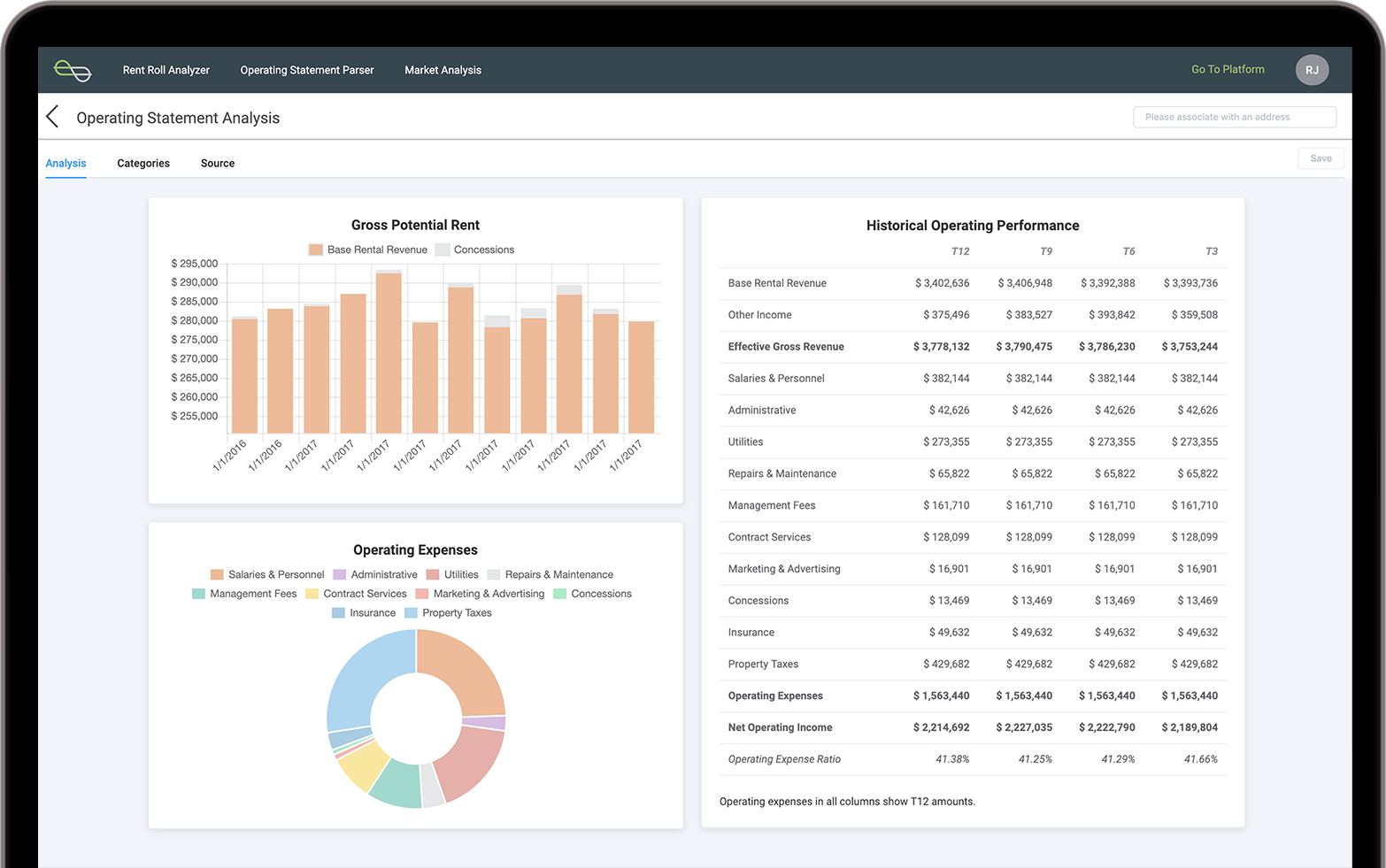

Enodo is a multifamily underwriting platform powered by artificial intelligence (AI) that enables underwriters to bring their real estate survey to a new level, find more investment opportunities for lenders, and track their underwriting process.

Enodo dashboard

Enodo speeds up the deal flow by helping underwriters perform calculations with impeccable precision, choosing accurate property comparables, and evaluating deals in minutes with built-in AI.

| Features | Cons |

|---|---|

🔹Founded: 2000

🔹Location: Overland Park, US

🔹Pricing: Pricing is customized based on your team’s specific needs

Archer

Archer is a predictive acquisitions solution that assists companies in underwriting and deal sourcing.

The software helps a user compare the real estate submarkets and choose the one that aligns the best with their investment strategy.

With baked-in Auto Comps, Accelerated Underwriting, and Benchmarking, a user can build a deal pipeline and underwrite it in a matter of minutes.

| Features | Cons |

|---|---|

🔹Founded: 2009

🔹Location: Laguna Niguel, US

🔹Pricing: Subscription based, $129 per user per month (monthly subscription)

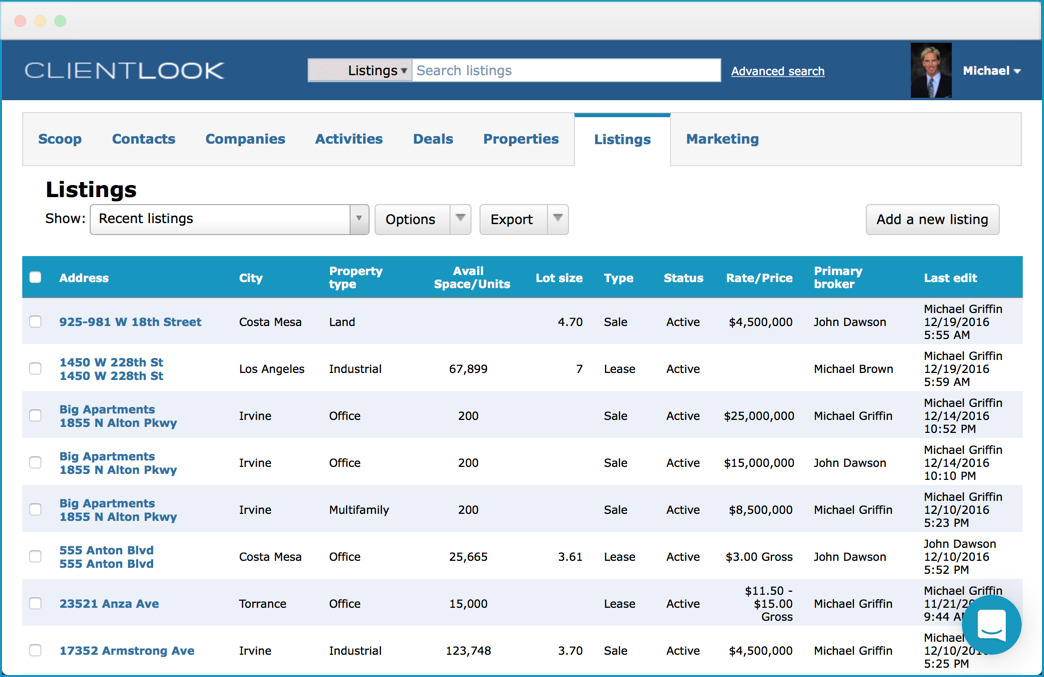

ClientLook is a commercial underwriting platform that combines CRM functionality with deal management tools to help brokers, investors, and underwriters. ClientLook attracts professionals by its ability to consolidate contact management, deal tracking, and property data.

ClientLook dashboard

For underwriters, ClientLook offers tools to track property performance, manage investor communication, and store essential documentation, such as financial statements, lease details, and appraisal reports. Such a centralized storage ensures that all relevant data is easily accessible.

| Features | Cons |

|---|---|

🔹Founded: 1971

🔹Location: Solon, US

🔹Pricing: 14-day trial. Subscription plans: $599 for small, $1680 for medium, $300 for large, and custom (billed annually)

MRI Contract Intelligence

MRI Contract Intelligence is an AI-based commercial underwriting platform that focuses on automating the extraction of data from leases and contracts. It’s designed to help underwriters quickly find essential information in legal documents without the need for manual review.

This commercial underwriting software automatically identifies and organizes key terms such as rent escalations, renewal options, and termination clauses. This helps real estate professionals quickly review and analyze large sets of lease data without having to search through each document manually.

| Features | Cons |

|---|---|

🔹Founded: 1995

🔹Location: Woodbridge, US

🔹Pricing: to be enquired

VisualLease

VisualLease is a lease management and accounting solution. As a commercial underwriting platform, it helps underwriters efficiently manage lease portfolios while ensuring compliance with accounting standards like ASC 842 and IFRS 16.

The platform is well-suited for businesses with complex leasing structures. It offers centralized lease data, automated workflows, and financial reporting to simplify lease management.

| Features | Cons |

|---|---|

🔹Founded: 2015

🔹Location: Toronto, Canada

🔹Pricing: Cost varies based on transaction volume, user count, and required features

U-Rite

U-Rite is a commercial underwriting platform that provides advanced tools for evaluating and managing commercial real estate (CRE) transactions.

The platform integrates directly with Excel. Users can perform detailed commercial real estate calculations and create discounted cash flows (DCFs) within Excel, with real-time updates between U-Rite and Excel workbooks.

The commercial underwriting software handles multi-property portfolios and is designed for both acquisition and development projects. It provides advanced tools for analyzing leases and recoveries and supports detailed financing and debt schedule modeling. U-Rite also automates the extraction of rent roll data, making it easier to organize and review rent information.

| Features | Cons |

|---|---|

🔹Founded: 2019

🔹Location: Singapore

🔹Pricing: 14-day trial with custom subscription plans

Docsumo

Docsumo is an advanced commercial underwriting platform that automates the extraction of data from various documents with no manual setup. This commercial underwriting software helps with processing a range of commercial real estate (CRE) documents, including T12 statements, offering memorandums, and operating statements, making the underwriting process more efficient.

The platform offers automated data extraction, eliminating the need for manual data entry. Docsumo features auto-classification to easily categorize different document types and robust data validation tools to ensure accuracy.

| Features | Cons |

|---|---|

Determining when to invest in a custom commercial underwriting software can be crucial for optimizing your operations. Here are some key scenarios where a custom solution may be more beneficial than an off-the-shelf option.

Apart from poor customer service, it sometimes happens that a company whose services you’ve subscribed to stops updating the software. In the end, you get a tool that jeopardizes your data security and doesn’t meet industry standards. Meanwhile, with a bespoke software, your company´s IT team is fully in charge of changes.

Sure, developing a custom CRE system is a costly decision in the short term, that’s why switching to a pre-built solution might help you cut back on expenses. But in the long run, you’ll have to pay for annual subscriptions, and checks will pile up. Meanwhile, you pay for a custom-made solution once and for all and forget about writing checks.

Unfortunately, off-the-shelf tools are infamous for restricted functionality and low customization capabilities. Plus, you’ll never own pre-built software.

With a custom underwriting solution, there is always room for customization if your business expands. Also, you don’t want to overpay for the features underwriters aren’t using – a custom CRE underwriting system will include only the functionality that is part and parcel of your daily underwriting activities.

If you’ve already got loan origination, compliance, appraisal, and document management tools, you might want to synchronize them. An off-the-shelf solution won’t fully integrate with all your company’s tools, while a custom CRE will be designed in a way to accommodate a large-scale integration with legacy systems.

Digitalized workflows are a basis for closing more deals, having fewer errors, and saving time on manual data entry.

We’ve been helping real estate companies automate their business processes with digital solutions that bring value, save costs, and grow revenue.

Why choose Ascendix?

How Ascendix can integrate AI into your commercial real estate operations:

Let’s optimize your commercial real estate underwriting operations with a digital solution to fine-tune your workflow and save you time!

“ I think the advantage that Ascendix has is that we're not trying to boil the ocean, meaning we're not trying to solve everybody's problems. We are very discreetly and intentionally going after the real estate sector. ”

Real estate underwriting software is a type of digital solution used by underwriters for the automation of activities like financial data collection, its analysis, and calculations.

The most popular underwriting automation software on the proptech market is Clik.ai, followed by rDCF, RealInsight, Archer, and Enodo.

We are a team of software developers, data analysts, Proptech consultants, and AI experts from the United States and Europe. Since 1996, we've been helping companies make the most out of their software and automate business workflows leveraging advanced technology.

(28 votes, average: 4.50 out of 5)

(28 votes, average: 4.50 out of 5)Get our fresh posts and news about Ascendix Tech right to your inbox.

Pretty! This has been a really wonderful post. Many thanks for providing these details.